Federato Blog

Featured resources

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Video

Company News

Federato Customer Council: Building community to shape the future of insurance

May 29, 2026

Video

Media

Insurance Edge: Getting The Best Value From Your Data is More Important Than Ever

April 27, 2026

Video

Company News

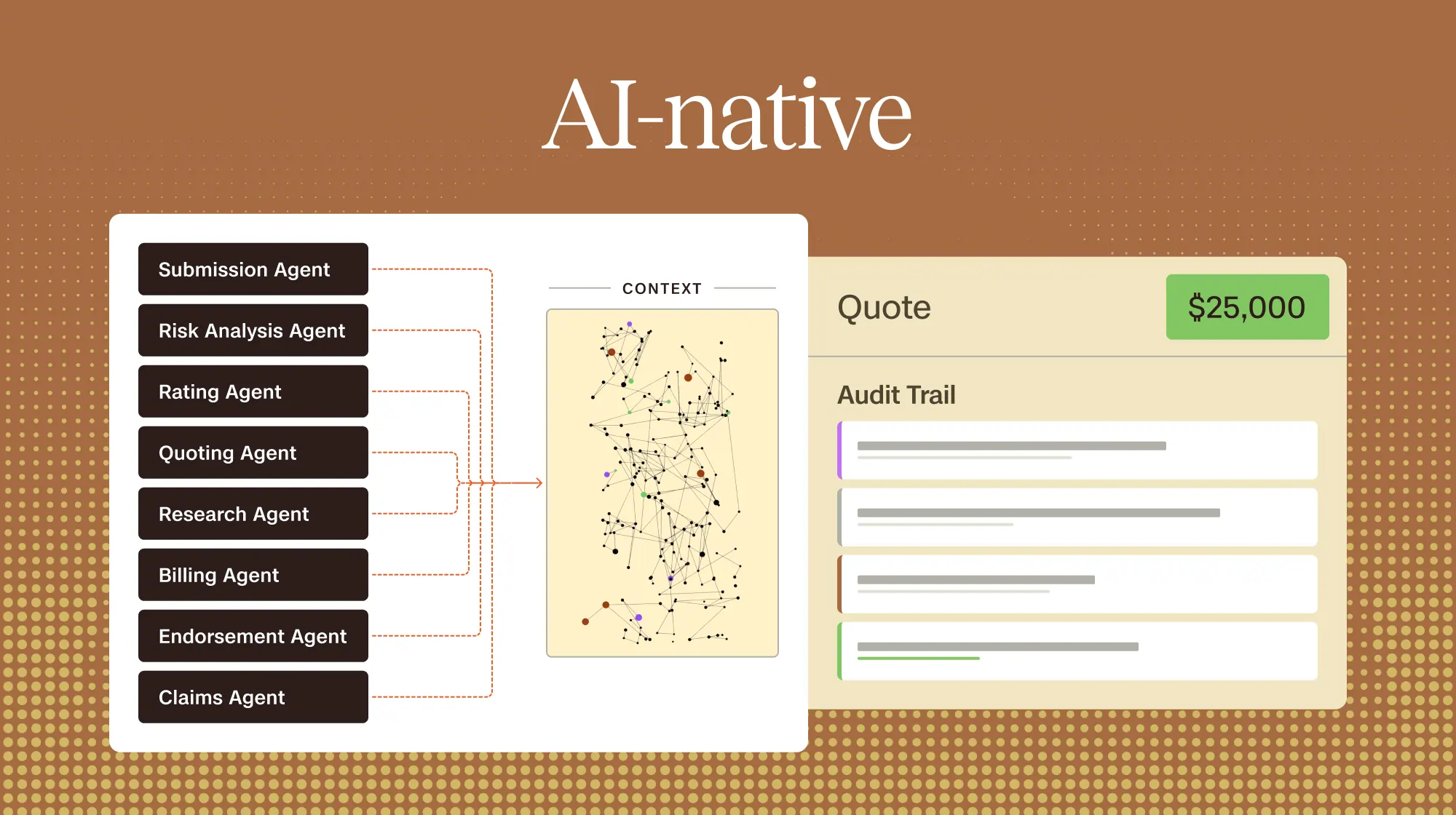

Introducing Product Studio: where product anchors the full policy lifecycle

April 15, 2026

Video

Company News

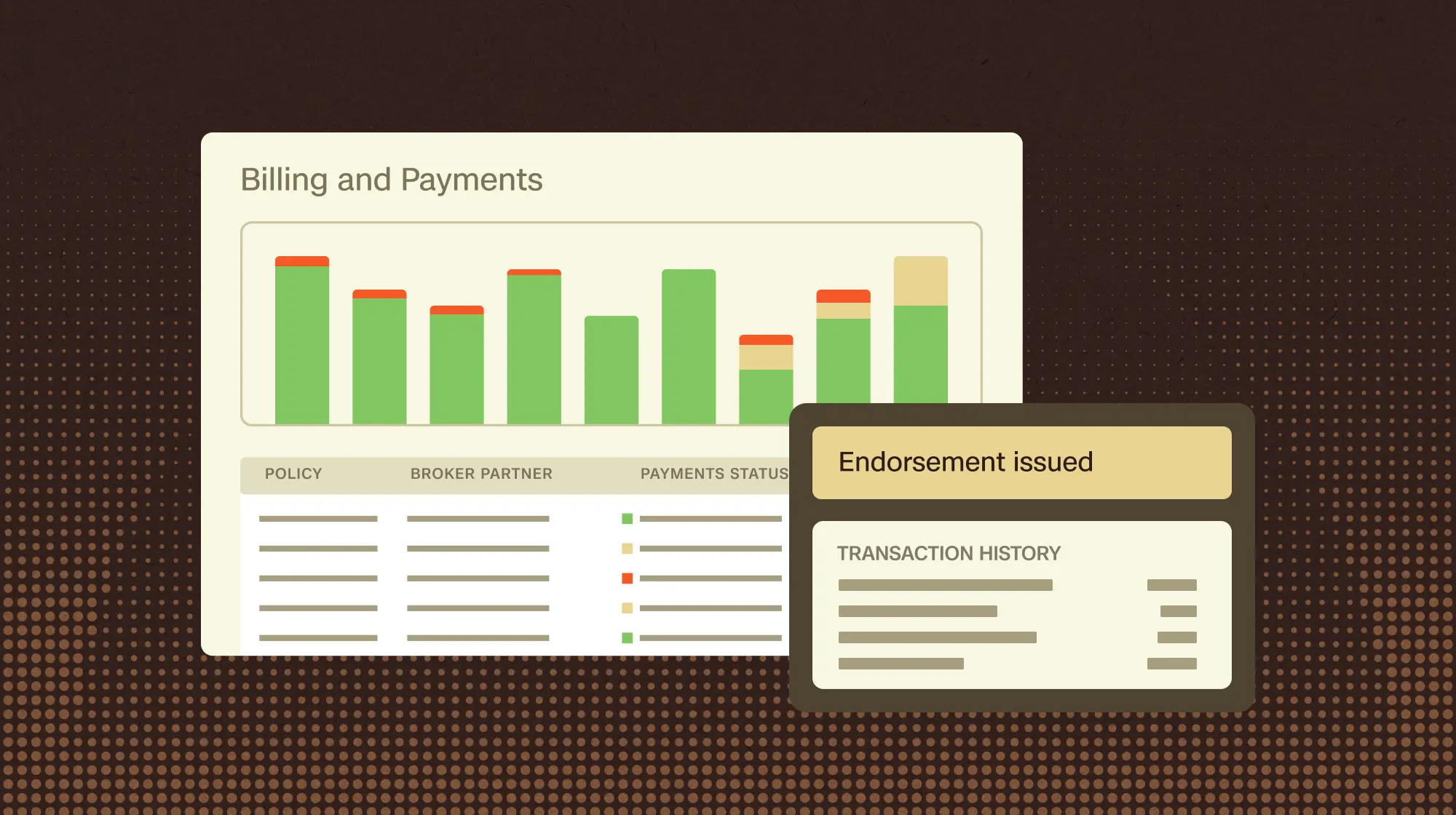

Federato Billing and Payments: real-time financial control built into the full policy lifecycle

March 31, 2026

Video

Insurance

Build reinsurer confidence through AI-native, full policy lifecycle execution

February 27, 2026

Video

Insurance

How full policy lifecycle operations modernize traditional insurance operations

February 6, 2026

Video

Case Study

MISSION accelerates program incubation and powers underwriting efficiency with Federato’s AI-native platform

January 29, 2026

Video

Insurance

3 ways industry leaders are transforming insurance for an AI-native future

January 28, 2026

Video

Company News

Content Management reimagined: centralizing account context across systems

January 8, 2026

Video

Insurance

The cost of doing nothing: why sticking with status quo is holding insurers back

December 30, 2025

Video

Media

The Software Leaders Uncensored Podcast: William Steenbergen talks AI-native insurance and engineering at scale

December 23, 2025

Video

Company News

Federato appoints Lisa Khoury as Chief Marketing Officer to accelerate AI-native insurance transformation

December 17, 2025

Video

Company News

Schema Sense: AI-native tooling that creates trusted data pipelines at unmatched speed

December 15, 2025

Video

Insurance

How carriers leverage portfolio visibility to align underwriting decisions with strategy

December 12, 2025

NO RESULT FOUND.

Ready to get started?